宽客财经

关注微信公众号"宽客财经",定时推送前沿、专业、深度的交易极客和量化投资资讯。

搜索

关注微信公众号"宽客财经",定时推送前沿、专业、深度的交易极客和量化投资资讯。

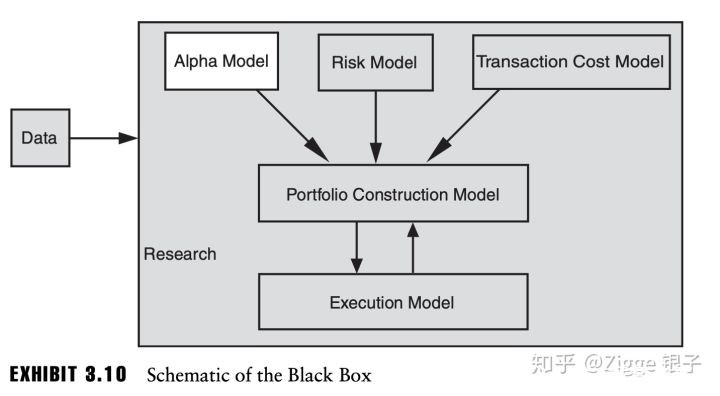

概念交易结构:Alpha+风险+交易成本 -》投资组合-》执行模型。 前三个都只是指导交易,像是你在做交易决定前必须要询问的大师。通过结合这三方意见来得出你现在最佳的投资组合,然后再去市场上用执行模型进行交易最终达到目标组合。

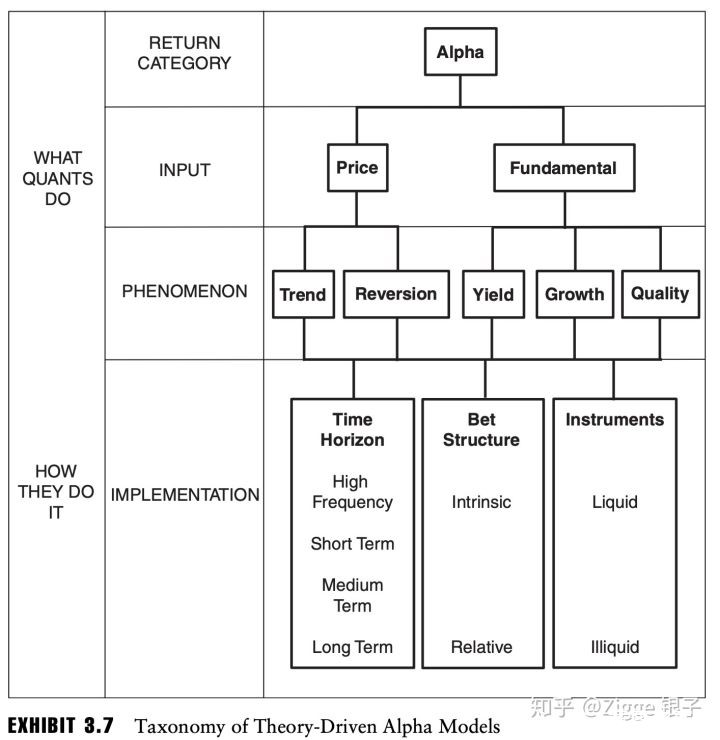

* Alpha: 不属于标准衡量的投资**入,单单属于投资策略创造的**入。一般用Alpha作为一种手段来衡量投资人的区别于市场变化的独立的投资策略好坏。

Alpha - 五大策略理论:趋势,反转,价值,增长,质量。其中第一二种用到价格相关数据,其余的用到基本面数据。

风险(factor related):风险就是那些你在设计模型初压根没有想到的因子。假设我们用消费者粘度QLS排名了一系列公司,第一名是苹果,最后一名是南山乳业。所以我们的策略就是买苹果**牛奶。我们的风险是什么?风险是你没考虑的因素。苹果属于高科技产业,而南山属于消费品产业(产业不同)。苹果是美国的,南山是中国的(地理不同)。有可能未来经济危机或者世界大战无人再去投资高科技,未来中国崛起干掉美国。于是你亏了很多。注意每一则统计结论都是开始于这段话:假设其他因子保持不变的情况下。风险就是其他因子变化的情况下。很显然,你的结论就是不可靠的。 那怎么办?如果你够强你可以发现风险因子(产业,地理)并且预测他们未来的走势,你就可以直接把潜在风险变成Alpha了(risk & alpha本来就是一个**的两面)! 但是更多时候你根本不知道为什么你之前一直盈利的策略突然就不赚钱了(不知道风险是什么),并且即使你知道了你也无法准确预测。咋办? 对冲咯(hedge)。ok,我知道苹果属于高科技产业并且是在美国,那我买苹果,我就**华为。**华为这个举动即对冲了你的产业风险,也对冲了你的地理风险。换句话说在消费者粘度,产业,地理这个三维世界里你通过对冲掉产业,地理降维到了只有消费粘度的一维线性世界,只有这时候你才可以安全的进行线性排序(QLS)重新回到你的“every other thing stays equal”假设。 如何去识别风险呢? PCA - 我知道苹果的波动80%来自于美国股市的整体波动。注意风险识别也是一个时间序列-不同时间段里面的风险来自于不同因子。比如说最近石油价格成为了投资者的关注重点。于是苹果的波动在最近可能40%来自于石油波动。 P.s这里说的风险属于因子类型,另外一种风险是价格波动风险(价格标准差,maxDrawDown等)。我会倾向于把前者说成后者的原因。 如何衡量一个策略的好坏 1. 利润:累计利润时间图 2. 稳定程度:MaxDrawDown 3. 预测:R^2 (0.05 就算牛逼了) 4. 时间延迟:如果获得信息输入时间延迟会对结果产生什么影响? 如何做实时监视: 1. 我们赚钱了么? 2. 我们是怎么赚钱的? * 实现了的利润 * 未实现的利润:有些策略会很快的终止损失单,很慢的终止盈利单。如果你看到你又一个损失单持续了5个消失,你要思考为什么。 3. 单子执行了么? 方法The trading system has three modules—an alpha model, a risk model, and a transaction cost model—which feed into a portfolio construction model, which in turn interacts with the execution model. Given data, quants can perform research, which usually involves some form of testing or simulation. Through research, the quant can ascertain whether and how a quant strategy works. They come up with ideas, test strategies, and decide which ones to use, what kinds of instruments to trade, at what speed, and so on. Humans also tend to control a “panic button,” which allows them to reduce risk if they determine that markets are behaving in some way that is outside the scope of their models’ capabilities. 记录巴菲特在长时间内打败了市场。但是在上世纪九十年代后期的互联网泡沫里他的策略表现的并不好。 Long Term Capital Management(LTCM)在1998年八月到十月期间损失了所有资本(在这之前的四年前期间平均**益30%)。 The TABB Group, a research and advisory firm focused exclusively on the capital markets, estimates that, in 2008, approximately 58 percent of all buy-side orders were algorithmically traded. TABB also estimates that this figure has grown some 37 percent per year, compounded, since 2005. The Barclay Group, proprietor of the most comprehensive commercially available database of CTAs and CTA performance, estimates that well over 85 percent of the assets under manage- ment among all CTAs are managed by quantitative trading firms. 鸡血why being a quant The first reason it is useful to study quants is that they are forced to think deeply about many aspects of their strategy that are taken for granted by nonquant investors.You have to specify what find means, what cheap means, and what stocks are. For example, finding might involve searching a database with information about stocks and then ranking the stocks within a market sector (based on some classification of stocks into sectors). Cheap might mean P/E ratios, though one must specify both the metric of cheapness and what level will be considered cheap. As such, the quant can build his system so that cheapness is indicated by a 10 P/E or by those P/Es that rank in the bottom decile of those in their sector. And stocks, the universe of the model, might be all U.S. stocks, all global stocks, all large cap stocks in Europe, or whatever other group the quant wants to trade.All this defining leads to a lot of deep thought about exactly what one’s strategy is, how to implement it, and so on. I have been in countless meetings with discretionary traders who, when I asked them how they decided on the sizes of their positions, responded with variations on the theme of, “Whatever seemed reasonable.” This is by no means a damnation of discretionary investment styles. I merely point out that precision and deep thought about many details, in addition to the bigger-picture aspects of a strategy, can be a good thing, and this lesson can be learned from quants. Perhaps the most obvious lesson we can learn from quants comes from the discipline inherent to their approach. Upon designing and rigorously testing a strategy that makes economic sense and seems to “work,” a properly run quant shop simply tends to let the models run without unnecessary, arbitrary interference. In many areas of life, from sports to science, the human ability to extrapolate, infer, assume, create, and learn from the past is beneficial in the planning stages of an activity. But execution of the resulting plan is also critical, and it is here that humans frequently are found to be lacking. A significant driver of failure is a lack of discipline.Many successful traders subscribe to the old trading adage, “Cut losers and ride winners.” However, discretionary investors often find it very dif- ficult to realize losses, whereas they are quick to realize gains. 免责申明:本文内容(包括但不限于文字,图片等内容)来自网络或者宽客之家社区用户发布,仅代表作者本人观点,与本网站无关。本网站不对所包含内容的准确性、可靠性或完整性**任何明示或暗示的保证,并读者理性阅读,并自行承担全部责任!如内容不慎侵犯了您的权益,请联系告知,核实情况后我们将尽快更正或删除处理! |